“What counts in making a happy marriage is not so much how compatible two people are, but how they deal with incompatibility.” Leo Tolstoy

There was a world record of mergers and acquisitions in 2015. Seventy to eighty percent of all mergers and acquisitions are financial failures according to an article in the Harvard Business Review.

During 2015, Microsoft wrote off ninety-six percent of the value of the handset business it acquired from Nokia for $7.9 Billion in 2014. Google lost $2.9 Billion in the communication device business it purchased from Motorola. News Corporation sold MySpace for $35 Million after buying it for $580 Million just six years earlier.

How much value the buyer is willing to put into the deal determines how much value will come out of the purchase over the long-run.

Harvard’s research shows that when a company is intent on purchasing a business with their sole focus on what they are going to get versus what new value they can create, the transaction usually ends with disastrous results for both the buyer and the seller.

The seller can elevate the cost to the buyer in a number of ways that ends up destroying all of the potential value to the buyer. This is especially true when there are one or more suitors interested in the same company at the same time.

Strategic Partnership Benefits

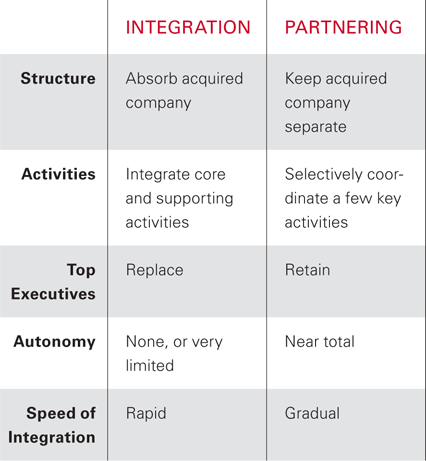

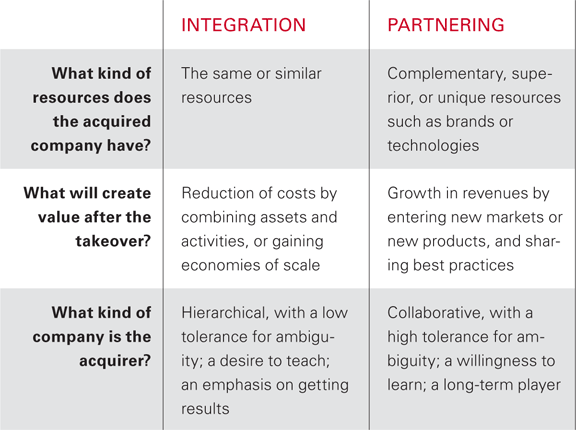

We believe a buyer’s goal should be to partner with the business it plans on purchasing in a collaborative way. It must add value for all the parties to the transaction rather than simply trying to control the other company.

The acquirer can form a strategic partnership with the seller to add value by providing strong cultural values, growth capital, better management oversight and unique talents and skills that were not present or available before the purchase. The chart below highlights the benefits in a partner versus an integration based acquisition.

Source: hbr.org

Acquisition Method

Once the acquisition agreement has been finalized, it must be accounted for according to United States Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) as shown below.

Measure:

- all tangible assets and liabilities that were acquired

- all intangible assets and liabilities that were acquired

- the amount of any non-controlling interest in the acquired business

- the amount of consideration paid to the seller

- any goodwill or gain from the transaction

Fair Value Principle

The “Fair Value Principle” is intended to provide greater accuracy in reporting the acquisition’s effect on an investor’s equity share because it values the transaction including any contingencies on the final acquisition date rather than during the time between the acquisition announcement and its final settlement.

“Fair value” is defined as the value a third party would freely pay for the assets and liabilities involved in the acquisition. If the “fair value” is more than the purchase price, it is considered a “bargain price” and is treated as a gain on the acquirer’s Income Statement. If the “fair value” is less than the purchase price, the difference must be reported as an intangible asset called “goodwill” on the purchaser’s Balance Sheet.

The acquisition method views the purchase as a whole rather than just the sum of its parts. Consequently, it requires all contingencies (defined as assets and liabilities that are “more likely than not” to be recognized in the future) be fully disclosed. For example, any potential lawsuits, product warranties or financial obligations that could have a material effect on the future of the business must be reported at their “fair value” on the date of acquisition.

The financial effects of acquisitions can be very complex. It is highly recommended that you consult with a professional before embarking on this journey.

How We Can Help You

Pacific Crest Group (PCG) provides professional services that keep your business focused on your critical objectives. We provide strategic Accounting and Human Resource (HR) services created specifically to help you meet your goals. Through exemplary customer service, clearly defined policies and procedures as well as a forward looking perspective, we provide the outsourced solutions your business needs to grow. A PCG professional is happy to meet with you to discuss solutions for your unique requirements designed to maximize all of your business opportunities.